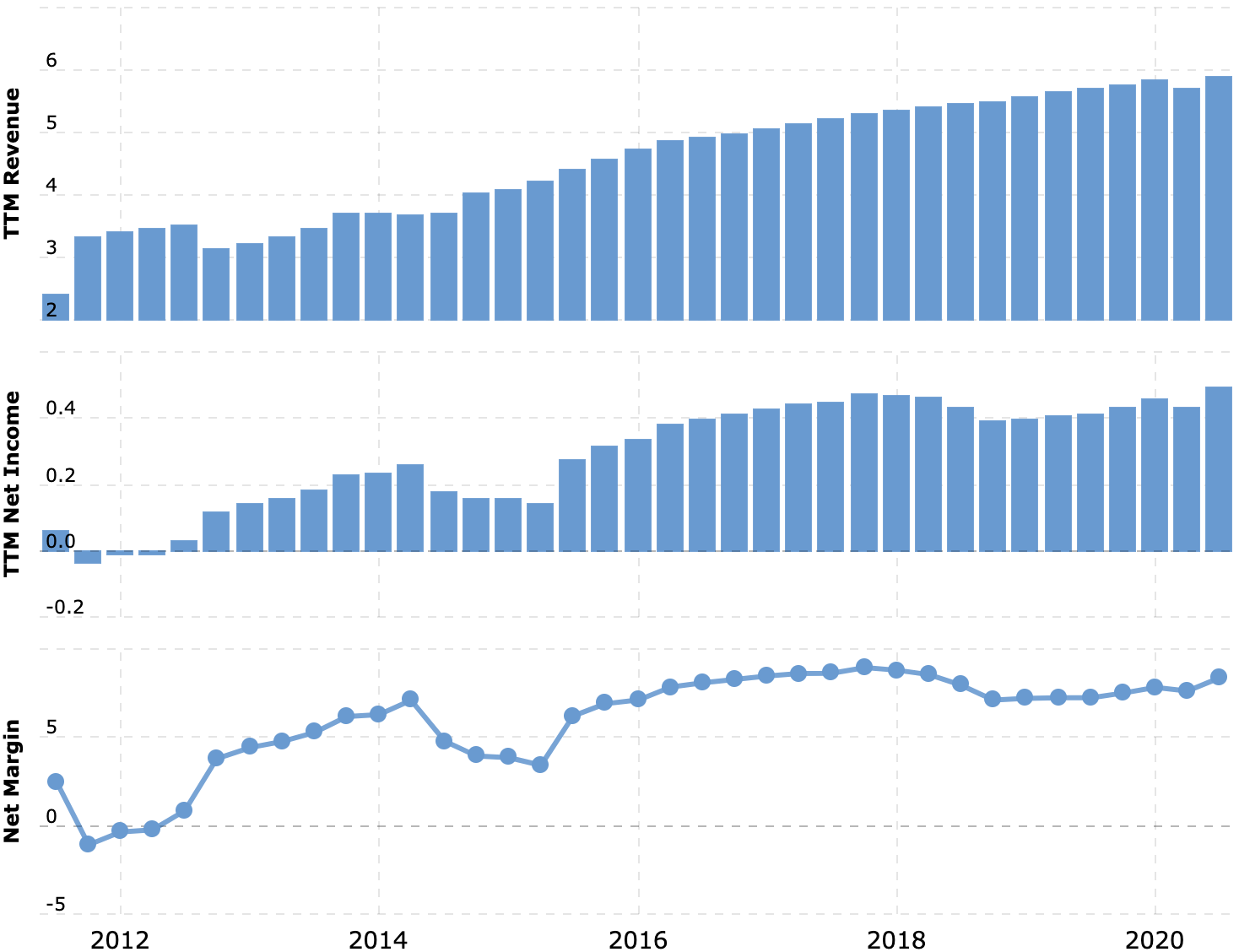

Fortune Brands Home & Security (NYSE: FBHS) is an American manufacturer of home improvement products. The company has been able to capitalize well on the American economy. And it may yet be able to capitalize on it.

What they make money on

The company is engaged in the production of home furnishings products. According to the annual report, revenue is divided into three segments:

- Cabinets. For kitchens, bathrooms and other rooms in homes.

- Plumbing. These are taps, sinks, etc.

- Doors and Security. Steel and fiberglass doors, locks, electronic security systems.

The authors of the report were kind enough to describe not only which segments bring in how much revenue, but also what their profitability is. Most of the revenue is made by the company in the United States.

The company’s main sales come from wholesalers – in fact, the company works for home builders and convenience stores.

Company revenue by segment in millions of dollars

| 2018 | 2019 | Percentage difference | |

| Cabinets | 2418,6 | 2388,5 | −1,2% |

| Plumbing | 1883,3 | 2027,2 | 7,6% |

| Doors and security | 1183,2 | 1348,9 | 14,0% |

| Total | 5485,1 | 5764,6 | 5,1% |

The company’s operating profit by segment in millions of dollars

| 2018 | 2019 | Percentage difference | |

| Cabinets | 143,5 | 178,3 | 24,3% |

| Plumbing | 375,3 | 427,6 | 13,9% |

| Doors and security | 155,6 | 172,3 | 10,7% |

| Intra-corporate settlements | −79,2 | −79,7 | −0,6% |

| Total | 595,2 | 698,5 | 17,4% |

Source: Company’s annual report, p. 16 (18)

Company sales by region

| Millions of dollars | Interest on revenue | |

| USA | 4823,9 | 84% |

| Canada | 401,0 | 7% |

| China | 355,4 | 6% |

| Other countries | 184,3 | 3% |

| Total | 5764,6 | 100% |

Source: Company’s annual report, p. 14 (16)

Company revenue by sales channel in millions of dollars

| 2018 | 2019 | |

| Wholesale customers | 2607,3 | 2682,8 |

| Building material stores | 1452,3 | 1606,7 |

| Other Stores | 311,6 | 304,8 |

| Builders, direct sales | 235,4 | 229,4 |

| U.S. sales overall | 4606,6 | 4823,7 |

| International Sales | 878,5 | 940,9 |

| Total | 5485,1 | 5764,6 |

Source: Annual Report, pp. 53 (55)

Positive conditions in all directions

The U.S. real estate market is feeling great: new home sales, mortgage applications, construction rates in all regions of the country are up, and more building permits are being issued.

This is a definite plus for Fortune. In fact, the company’s results in 2020 confirm this: in spite of the coronary crisis difficulties in the first half of the year, it was a positive year for the company as a whole.

The company is also benefiting from the deteriorating crime situation in the U.S., since a significant part of its revenue is from home security products. In principle, we have already covered this subject well in our ideas on Napco, Allegion, Resideo, and Alarm.com. We can only add that the events of the last few months – the storming of government buildings, the information blockade of the incumbent president – have only confirmed our point. Therefore, in the long term, the “security” segment of Fortune will still prove itself.

Financial indicators of the company for the period of 3 months in millions of dollars

| 1 Jul – 30 Sep 2019 | 1 Jul – 30 Sep 2020 | |

| Revenue | 1459,0 | 1652,1 |

| Cost of goods | 934,8 | 1071,5 |

| Sales, general and administrative expenses | 311,3 | 328,3 |

| Amortization of intangible assets | 9,9 | 10,5 |

| Loss of asset value | 29,5 | – — |

| Restructuring costs | 5,5 | 1,6 |

| Operating profit | 168,0 | 240,2 |

| Interest payments | 23,6 | 20,1 |

| Other income | −0,3 | −2,1 |

| Profit before tax | 144,7 | 222,2 |

| Income tax | 39,0 | 54,0 |

| Profit after tax | 105,7 | 168,2 |

| Losses of subsidiaries | – — | 2,4 |

| Total profit | 105,7 | 165,8 |

Financial indicators of the company for the period of 9 months in millions of dollars

| 1 Jan – 30 Sep 2019 | 1 Jan – 30 Sep 2020 | |

| Revenue | 4294,1 | 4430,6 |

| Cost of goods | 2773,5 | 2873,9 |

| Sales, general and administrative expenses | 943,9 | 918,4 |

| Amortization of intangible assets | 30,0 | 31,1 |

| Loss of asset value | 29,5 | 22,5 |

| Restructuring costs | 11,2 | 16,5 |

| Operating profit | 506,0 | 568,2 |

| Interest payments | 71,8 | 64,4 |

| Other income | −2,2 | −13,4 |

| Profit before tax | 436,4 | 517,2 |

| Income tax | 109,1 | 121,7 |

| Profit after tax | 327,3 | 395,5 |

| Losses of subsidiaries | – — | 4,7 |

| Total profit | 327,3 | 390,8 |

Source: Company’s quarterly report, p. 2

Financial indicators of the company for 3 months by segments in millions of dollars

| 2019 | 2020 | Percentage difference | |

| Revenue in the “Plumbing” segment | 514,1 | 590,6 | 14,9% |

| Revenue in the Doors and Security segment | 355,2 | 406,7 | 14,5% |

| Revenue in the “Cabinets” segment | 589,7 | 654,8 | 11,0% |

| Total revenue | 1459,0 | 1652,1 | 13,2% |

| Operating profit in the “Plumbing” segment | 112,0 | 116,6 | 4,1% |

| Operating profit in the Doors and Security segment | 50,1 | 66,8 | 33,3% |

| Operating profit in the “Cabinets” segment | 25,1 | 82,1 | 227,1% |

| Intra-corporate settlements | −19,2 | −25,3 | −31,8% |

| Total operating profit | 168,8 | 240,2 | 43,0% |

Financial indicators of the company for 9 months by segments in millions of dollars

| 2019 | 2020 | Percentage difference | |

| Revenue in the “Plumbing” segment | 1478,8 | 1564,4 | 5,8% |

| Revenue in the Doors and Security segment | 1017,6 | 1052,7 | 3,4% |

| Revenue in the “Cabinets” segment | 1797,7 | 1813,5 | 0,9% |

| Total revenue | 4294,1 | 4430,6 | 3,2% |

| Operating profit in the “Plumbing” segment | 307,9 | 330,6 | 7,4% |

| Operating profit in the Doors and Security segment | 122,5 | 143,5 | 17,1% |

| Operating profit in the “Cabinets” segment | 134,0 | 163,1 | 21,7% |

| Intra-corporate settlements | −58,4 | −69,9 | −18,2% |

| Total operating profit | 506,0 | 568,2 | 12,3% |

Source: Company Quarterly Report, page 19. 19

It’s not all that great.

But there are a number of subtleties that can cause stocks to fall.

Concentration. According to the annual report, the company has two major buyers: Home Depot and Lowe’s. They each account for 14% of revenue. A hypothetical renegotiation with these large customers could ruin the company’s bottom line.

This holiday will come to an end someday. The U.S. real estate market has already performed a miracle a few times in 2020, renewing sales records during the recession, and we shouldn’t expect it to continue indefinitely: the first symptoms of decline are already appearing. Although more homes are being built, builders’ confidence levels are falling due to rising costs of building materials and the costs associated with the coronary crisis. It could be that construction activity in the U.S. will soon decline, and that will have a negative impact on Fortune’s reporting.

The dividend drinkers are nothing but trouble. The company pays $1.04 in dividends per share a year, which, with a current stock price of $87.37, yields an annual rate of 1.19%. It costs the company about $135 million a year – about a third of its profits. The company has quite a lot of debt: $3.89 billion, of which $1.135 billion has to be repaid within a year. In principle, the money at the company’s disposal should be enough for everything, but force majeure is possible, which will lead to a cut in dividends and a drop in shares.

Summary

Fortune is an interesting and promising issuer. On February 2, the company is releasing its report for the past quarter. You can take this stock ahead of the report to capitalize on the growth of the U.S. real estate market. The company’s price is sane: P/E is 24.87, – so there’s room to grow.